Audit

This website contains information on a MANDATORY DEADLINE that is due August 12, 2026. Please read this website in its entirety. If you have questions, inquire with the VP Finance at vpfinance@skule.ca IMMEDIATELY.

Financial audit

Per the Finance Policy §7.0.4, all Affiliated Clubs and Discipline Clubs are required to submit their financial records for the immediately preceding fiscal year to the Audit Committee for audit. This audit process ensures:

- Affiliated Clubs and Discipline Clubs are ultimately held accountable to the student community;

- Affiliated Clubs and Discipline Clubs operate on a non-profit basis;

- Affiliated Clubs and Discipline Clubs maintain records pursuant to the Finance Policy §7.0.1;

- All EngSoc funds are used for their approved purpose.

As the year 2026-7 is the first year audits are being conducted, the Audit Committee will not impose consequences on clubs that do not possess complete records of receipts. This exemption will not apply in subsequent years.

Audit cycle

The audit cycle is annual and runs from May to April.

For 2026-2027:

- In May 2026,

- Clubs will be informed that they must send financial statements and a specific audit report to the Committee;

- The report template will be issued for clubs to fill;

- The Audit Committee will be struck.

- In June 2026,

- Reports from all clubs are due on June 30.

- Clubs that are slated to be audited in July will be notified that they will be audited.

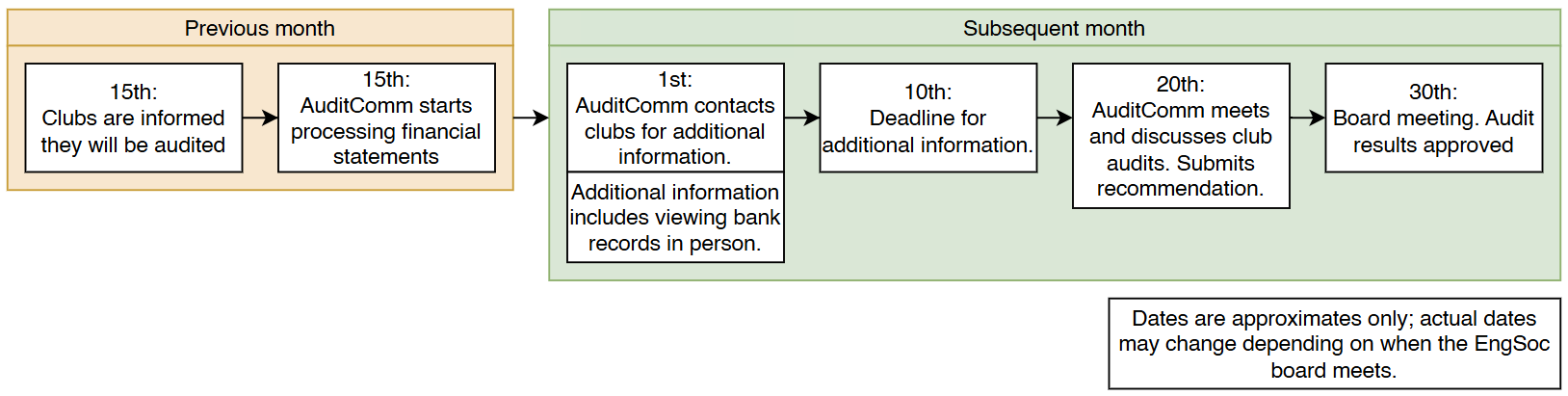

- In each subsequent month (except December and April):

- Clubs will be notified at a given month when it’s their turn to be audited the next month. Each audit cycle lasts one and a half months.

- AuditComm will start processing financial statements in the middle of a given month.

- If AuditComm requires additional information as part of the audit, including viewing bank statements and records in person, requests will be sent out early on the subsequent month.

- Any additional information will be due early-mid the subsequent month. AuditComm will resume the audit.

- All audits will conclude by the AuditComm meeting mid-late subsequent month, where a recommendation is produced for the Board to review.

- The Board reviews and approves audit results.

- Exact deadlines for each month will be confirmed by AuditComm and the VPF.

The order in which clubs are audited will be randomized. Approximately 10 clubs will be audited each month. Levy groups and discipline club audits will be spread across the year.

Audit Committee

| Name |

Position |

| Kaiy Cao |

VP Finance |

| Yana Khurana |

Finance Secretary |

| Aaryan Fredrick |

Ombudsperson |

| Arthur Chen |

Board Representative |

| Justin Fang |

Finance Representative |

| Ryan Hammer |

Finance Representative |

| Charlie Therence |

At-Large Representative |

| Jaden Hinds |

At-Large Representative |

| Melissa Lin |

At-Large Representative |

| Joy Zhou |

At-Large Representative |

| Keting Trinh |

At-Large Representative |

| Auva Bagriz |

At-Large Representative |

Report template instructions

Access the report template here and two filled examples here. Both examples are written based on typical design team scenarios:

Report template

Filled example

Filled example 2

The report template revolves around the concept of activity codes. Club activities are categorized into activity codes in the “P&L” tab, though you are free to define additional activity codes as necessary. Each transaction done by your club should be assigned under exactly one corresponding activity code. However, there are restrictions on assigning codes:

- All income activity codes must start with a 6 (see “P&L” tab).

- Special projects, conference funding, and SEF income and expenses should be reported under its own activity code (AC-6600, AC-6700, AC-6300 respectively).

- CPSIF and Winter Club Funding income should be reported under its own activity code (AC-6100 and AC-6200 respectively)

The “P&L” tab should provide a month-by-month, high level view of revenue and expenditure.

The “Breakdown of P&L” tab should provide a more granular documentation of expenditure, for instance if your club has events or initiatives with multiple sub-budgets. All levy groups and clubs with cash flow >$20k per year MUST fill in this tab.

The “Special Projects Actuals” tab should provide an accounting of how Special Projects funds were used. All Special Projects revenues should be reported in this tab. All expenses that use Special Projects funds should be reported in this tab.

The “SEF Actuals” tab should provide an accounting of how SEF was used. All SEF revenues should be reported in this tab. All expenses that use SEF funds should be reported in this tab.

The “Conference Funding” tab should provide an accounting of how Conference Funding was used. All Conference Funding revenues should be reported in this tab. All expenses that use Conference Funding funds should be reported in this tab. As Conference Funding funds up to 50% of a conference’s expenses, additional income sources should be declared where appropriate.

The “Transaction List Report” tab should provide a list of all transactions, both incoming and outgoing, made on behalf of the club. This can either be from the club’s bank account or from individual bank accounts.

The “Reimbursement Recipient List” should provide a list of all the club’s individual beneficiaries, including club executives and members who have received transfers from either EngSoc or the club’s bank account.

Reporting requirements – due August 12, 2026

By August 12, 2026, all affiliated and discipline clubs must submit, for the time period between May 2025 – April 2026:

- Bank statements;

- Dated receipts for all transactions, organized into folders by month (e.g. all receipts for June 2025 belong to one folder);

- The club’s annual budget for the time period above;

- Any special financial arrangements or explanations the Club wishes to disclose to the Audit Committee.

All documents must be submitted to the application form below with:

- All bank statements for the year put into one folder;

- Receipts for one activity code should be put into the same folder. In addition, all clubs must fill the report template below. Detailed instructions and examples are located in the first tab of the template.

Submission form

Report template

If you are…

| A levy group... |

A non-levy group that received more than $50000 last fiscal year... |

A non-levy group that received less than $50000 last fiscal year... |

| You do not need to fill the "P&L" tab as your audit submission to Rhonda will be used. |

You must fill both the "P&L" and the "Breakdown of P&L" tabs.

The contents of "Breakdown of P&L" must contain a transaction-by-transaction breakdown.

The contents of "P&L" must be a summary of "Breakdown of P&L" grouped by discrete activity or initiative.

|

You do not need to fill the "Breakdown of P&L" tab.

Provide a breakdown of your transactions grouped by discrete activity or initiative. |

If you received any funding from…

| Conference funding |

Special projects |

SEF |

| You must fill in the "Conference Funding Actuals" tab. |

You must fill in the "Special Projects Actuals" tab. |

You must fill in the "SEF Actuals" tab. |

If you are a discipline club, you must fill in who authorized each transaction in the “Transaction List” tab.

Regardless, you must fill in the “Club Information”, “Bank Statements”, “Transaction List Report”, and “Reimbursement Recipient List” tabs.

Example

Suppose affiliated club ABC will be audited in August 2026.

- The VPF will issue the report template and instructions in May 2026.

- Club ABC must submit required documents by June 30, 2026.

- AuditComm will notify Club ABC that they will be audited mid-July 2026. No action need be taken at this time.

- AuditComm will notify Club ABC of any additional documents that need to be reported by late July or early August 2026. The exact date will be decided by AuditComm.

- Club ABC must supply additional documents by around August 10, 2026. The exact date will be decided by AuditComm.

- AuditComm will conclude Club ABC’s audit by around August 20, 2026. The exact date will be decided by AuditComm.

- The EngSoc Board of Directors will decide to approve Club ABC’s audit at the August Board Meeting.

Audit schedule for August 2026 Cycle:

AuditComm Meeting Date: Sunday, July 12th, 2026

Auditing Clubs informed: Tuesday, July 14th

Next Board Meeting: Thursday, July 23rd

Contacting clubs for more information: Sunday, July 26th

Deadline for answer from clubs: Wednesday, August 5th

Next AuditComm Meeting: Any day after August 12th; more details to follow.